Member content

Already a member? Sign in below

Ad market set to reach £36bn this year despite the possibility of real-terms decline

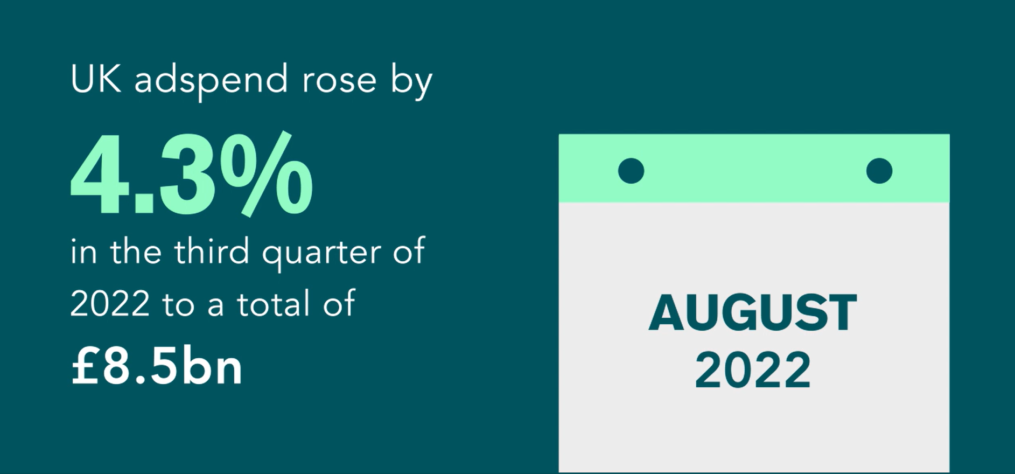

London, January 26, 2023: The latest quarterly data from the Advertising Association / WARC Expenditure Report show UK advertising spend rose by 4.3% to a total of £8.5bn between July and September 2022, the ninth consecutive quarter of growth and demonstrative of an ongoing, resilient recovery from the COVID-19 pandemic.

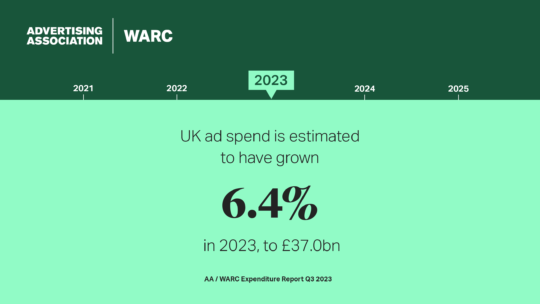

The UK’s ad market is expected to grow by a further 3.8% this year, totaling £36.1bn and following on from an estimated 8.8% rise in 2022, based on the latest advertising revenue data collected directly from media owners. The projection for 2023 is on par with the previous forecast (published in October 2022) but equates to a 3.0% real terms decline once inflation is accounted for. Forecasts for the coming year show reduced growth expectations for almost all sectors of advertising in line with pressures felt by all parts of the economy.

Q3 2022 results

Actual figures released by the Advertising Association/WARC for the first nine months of 2022 confirm that growth was up by 10.8%, with the total figure standing at £25.3bn. Out of Home (OOH) and cinema, specifically, continued their strong recovery during Q3, while search rose 7.7% – equating to almost 40% of total adspend during the quarter. Social media, included within online display, continued growing (+4.4%), while broadcast video on-demand (BVOD) spend rose by 4.3%.

Revised 2022 projections

The UK’s ad market is now thought to have reached a total of £34.7bn in 2022, as preliminary estimates put growth at 8.8% last year – this represents a slight downgrade of

-0.4pp from the October projections. After accounting for inflation, real growth was thought to have been flat in 2022, at -0.1%. Crucially, a retained recovery is projected for the ‘golden quarter’ (Q4 2022). Spend during this time was estimated to have grown by 4.0%, to a total of £9.5bn, as the winter period hosted the two biggest events for adspend: Christmas and the FIFA Men’s World Cup. This growth was still half a point behind previous forecasts but should nonetheless be considered as a good performance given economic challenges.

Stephen Woodford, Chief Executive, Advertising Association said:

“The UK advertising industry has held firm in its continued recovery from the COVID pandemic, with ad investment holding up in the face of significant headwinds. However, the economic pressures of 2022 including high inflation’s impacts on the wider economy and on media costs means in real terms spend is likely to be flat. These pressures all contribute to slower growth projections for the year ahead.

“Advertising plays a vital role in helping brands communicate with their customers and navigate the cost-of-living pressures that everyone faces. As we publish our new 3-year strategy which puts trusted, inclusive and sustainable advertising at the heart of our mission, we are determined to show the economic and social value of responsible advertising to the UK.”

James McDonald, Director of Data, Intelligence & Forecasting, WARC said:

“With the economy enjoying modest growth in November, and inflation appearing to have reached its peak, it is likely that the UK narrowly avoided slipping into the recession at the end of last year that many had feared – but a downturn now seems unavoidable in 2023.

“Despite an air of resilience in recent market results, a looming recession will put pressure on ad trade this year. We foresee ad market growth easing to 3.8%, equating to a real terms decline and the weakest rise in a decade if the pandemic-hit 2020 were excluded. The silver lining here is that our current modelling suggests that the slump will be short lived, with advertising investment set to lift by 5% over the first nine months of 2024.”

| Q3 2022 year-on-year % change |

2022 forecast year-on-year % change | Percentage point (pp) change in 2022 forecast vs October | 2023 forecast year-on-year % change | Percentage point (pp) change in 2023 forecast vs October | |

| Search | 7.7% | 11.7% | = | 6.2% | = |

| Online display* | 6.3% | 7.4% | +0.3pp | 5.4% | -0.5pp |

| TV | -6.6% | 0.9% | -2.0pp | 0.4% | -0.1pp |

| of which VOD | 4.3% | 10.5% | +0.4pp | 4.4% | -2.8pp |

| Online classified* | 7.2% | 20.9% | +0.8pp | -6.1% | -1.6pp |

| Direct mail | -4.7% | 1.8% | -1.0pp | -6.0% | -1.5pp |

| Out of home | 13.2% | 33.7% | +2.5pp | 5.8% | -1.0pp |

| of which digital | 13.3% | 33.2% | +0.9pp | 7.2% | -1.2pp |

| National newsbrands | -11.2% | 0.6% | -2.8pp | -4.8% | -2.3pp |

| of which online | -3.7% | 5.8% | -2.4pp | 1.0% | -2.7pp |

| Radio | -7.5% | 2.6% | -3.6pp | -0.2% | -0.3pp |

| of which online | -9.6% | 2.9% | -5.2pp | 6.0% | -0.3pp |

| Regional newsbrands | -10.4% | 0.4% | -2.2pp | -7.9% | -0.8pp |

| of which online | -6.6% | 4.0% | -3.2pp | -1.1% | -0.6pp |

| Magazine brands | -4.2% | 0.6% | -0.1pp | -6.4% | -0.5pp |

| of which online | -6.3% | 3.8% | -1.6pp | -0.9% | -0.8pp |

| Cinema | 148.1% | 148.6% | -25.4pp | 31.0% | +8.9pp |

| TOTAL UK ADSPEND | 4.3% | 8.8% | -0.4pp | 3.8% | -0.1pp |

| Note: *Broadcaster VOD, digital revenues for newsbrands, magazine brands, and radio station websites are also included within online display and classified totals, so care should be taken to avoid double counting. Online radio includes targeted in-stream radio/audio advertising sold by UK commercial radio companies, together with online S&P inventory.

Source: AA/WARC Expenditure Report, January 2023 |

|||||

The Advertising Association/WARC quarterly Expenditure Report is the definitive guide to advertising expenditure in the UK with data and forecasts for different media going back to 1982.

Already a member? Sign in below

If your company is already a member, register your email address now to be able to access our exclusive member-only content.

If your company would like to become a member, please visit our Front Foot page for more details.

Enter your email address to receive a link to reset your password

Your password needs to be at least seven characters. Mixing upper and lower case, numbers and symbols like ! " ? $ % ^ & ) will make it stronger.

If your company is already a member, register your account now to be able to access our exclusive member-only content.