UK adspend rose 28.3% to a total of £8.6bn in the first three months of 2022, 7.7 percentage points ahead of our previous forecast in April.

London, July 28, 2022: The latest Advertising Association/WARC Expenditure Report is the only source to collect advertising revenue data across the entire media landscape. It shows a strong Q1 for UK adspend with a year-on-year rise of 28.3%, reaching a total of £8.6bn and resulting in slightly improved outlooks for the year ahead. The first three months of 2022 outperformed expectations by 7.7 percentage points as all media recovered in comparison to the lockdowns of Q1 2021.

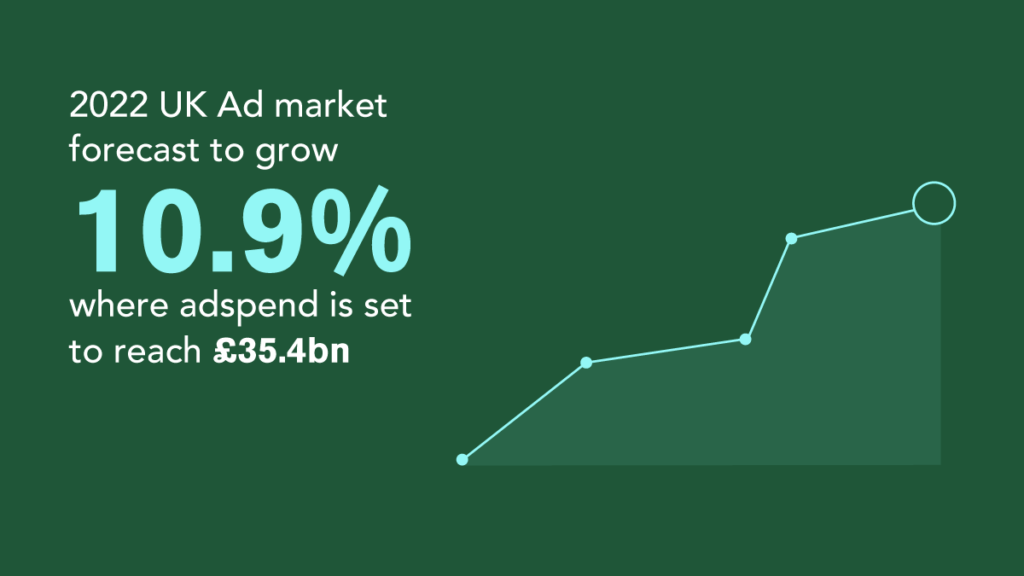

The outlook for the total UK advertising market in 2022 has been upgraded (+0.2pp) to 10.9% growth, by when adspend is set to reach a new high of £35.4bn. These figures also reflect the consistent growth of online advertising, which is forecast to account for 74.3% of all spend this year, in comparison to 73.5% in 2021.

Despite encouraging growth across most sectors, real growth in the UK’s ad market is expected to be just 1.8% this year when accounting for inflation. Erosion of margins due to increased costs may affect marketing budgets, with inflationary pressures likely to continue into 2023.

The latest dataset suggests the UK’s ad market will grow by a further 4.4% in 2023, to a value of £37bn. This represents a 1.0pp downgrade from AA/WARC’s April forecast, and equates to a 0.9% contraction in real terms. With inflationary pressures and issues faced by all businesses and families such as the rising cost of living – coupled with geopolitical uncertainties – the UK advertising market is liable to see further headwinds on the horizon.

Stephen Woodford, CEO, Advertising Association, commented: “It is encouraging to see growth in our industry over Q1, as the economy continues its recovery year-on-year following last year’s Covid-19 lockdown. However, the pressures of inflation on living standards and economic growth are at the top of everyone’s mind, and these rising costs may represent a real-term contraction of nearly 1% in 2023 for UK advertising investment.

“As the UK’s political leadership changes, it is important to recognise the value that advertising brings to the economy in supporting competition, innovation and growth at this critical time. A consistent, evidence-led policy-making approach, with due consideration of industry views and expertise, will help create the conditions which encourage, not hinder, economic growth and will be integral to the ability for businesses to weather the challenges of the coming year. Together with WARC, we will continue to monitor advertising expenditure results and provide guidance for our industry and policy decision-makers within the UK government.”

The full picture in Q1 2022

Data show that UK adspend rose by 28.3% in the first three months of 2022, as growth was recorded across all media. Online formats – notably search, display (including social) and classified – grew the most in absolute terms, as the market share reached 74.9% for online channels combined.

Triple and quad-digit recoveries were seen in the OOH and cinema sectors, respectively. The publishing and direct mail sectors also saw growth over these three months, resulting in improving outlooks for the year ahead. These figures are consistent with AA/WARC’s provisions for year-on-year growth.

Although these figures do show exponential growth, in comparison to Q1 2021, Covid-19 lockdown measures were still in place across the UK, diminishing advertising activities and revenue across the media landscape.

James McDonald, Director of Data, Intelligence & Forecasting, WARC commented: “The latest survey data show that the UK’s ad market is currently experiencing a soft landing from the turmoil caused by the Covid outbreak, with early budget commitments translating into a strong start to the year for the industry – all media recorded growth in the first quarter.

“As predicted, however, inflation is now starting to bite; its impact on the consumer is well documented, but the rising cost of servicing government debt leaves the incoming prime minister with less fiscal flex for stimulating flatlining economic activity. For advertisers, higher costs will carve into margins, and while a real term rise of 1.8% in ad investment is expected this year – compared to a pre-Covid average of +2.6% – the market is now set to contract in 2023 after accounting for these ongoing inflationary pressures.”

| Media | Q1 2022 year-on-year% change |

2022 forecast year-on-year

% change |

Percentage point (pp) change in 2022 forecast vs April | 2023 forecast year-on-year

% change |

Percentage point (pp) change in 2023 forecast vs April |

| Search | 29.9% | 13.2% | +1.0pp | 6.3% | -1.5pp |

| Online display* | 27.6% | 11.4% | -0.2pp | 6.7% | -0.7pp |

| TV | 19.1% | 5.9% | -1.2pp | 0.8% | -1.2pp |

| of which VOD | 25.9% | 13.3% | -1.2pp | 9.2% | -1.3pp |

| Online classified* | 29.9% | 5.6% | +2.6pp | -6.5% | -1.8pp |

| Direct mail | 15.6% | -0.2% | +3.9pp | -6.3% | +0.7pp |

| Out of home | 146.2% | 28.9% | -2.6pp | 10.9% | +2.3pp |

| of which digital | 142.8% | 30.5% | -3.8pp | 14.9% | +3.4pp |

| National newsbrands | 15.9% | 1.1% | +0.1pp | -1.8% | +1.0pp |

| of which online | 18.8% | 6.6% | +2.1pp | 2.7% | +1.8pp |

| Radio | 19.7% | 5.4% | +2.3pp | 2.1% | -1.7pp |

| of which online | 24.8% | 10.7% | -0.4pp | 8.6% | -0.8pp |

| Regional newsbrands | 22.2% | 0.0% | +4.8pp | -6.3% | +1.0pp |

| of which online | 25.8% | 8.0% | +4.4pp | 3.0% | +3.2pp |

| Magazine brands | 7.2% | -1.3% | +0.3pp | -4.2% | +1.1pp |

| of which online | 20.5% | 4.0% | +2.5pp | -0.2% | +1.9pp |

| Cinema | – | 191.2% | -21.8pp | 18.3% | +6.8pp |

| TOTAL UK ADSPEND | 28.3% | 10.9% | +0.2pp | 4.4% | -1.0pp |

| Note: Broadcaster VOD, digital revenues for newsbrands, magazine brands, and radio station websites are also included within online display and classified totals, so care should be taken to avoid double counting. Online radio includes targeted in-stream radio/audio advertising sold by UK commercial radio companies, together with online S&P inventory.

Source: AA/WARC Expenditure Report, July 2022 |

|||||

The Advertising Association/WARC quarterly Expenditure Report is the definitive guide to advertising expenditure in the UK with data and forecasts for different media going back to 1982.