SPEND PROJECTED TO NEAR £10BN DURING Q4 WORLD CUP CHRISTMAS PERIOD

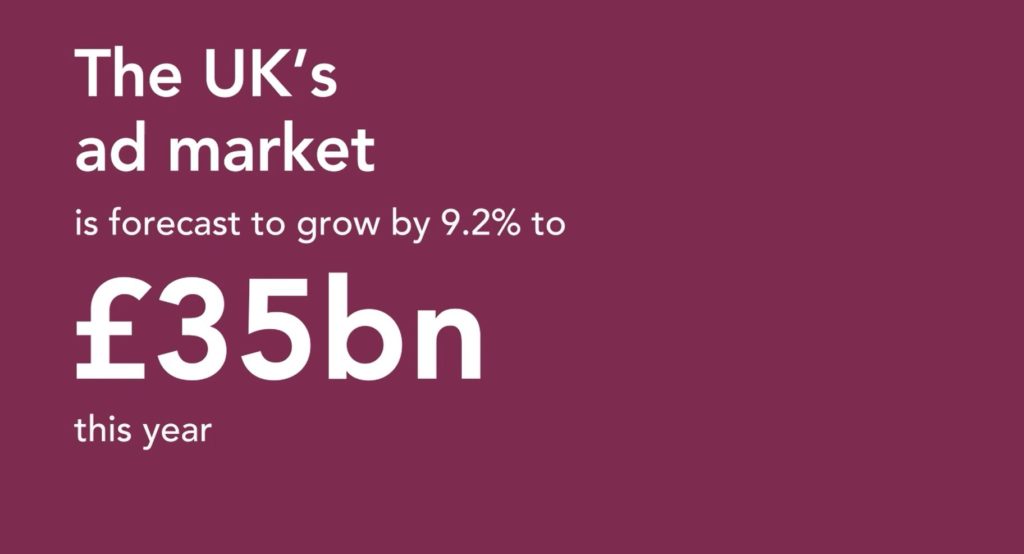

London, October 27th, 2022: The latest Advertising Association/WARC Expenditure Report has forecast the value of the UK’s advertising market will grow by 9.2% in 2022, to a total of £34.9bn, though this does reflect a downgrade of 1.7pp from the previous forecast in July. This revision is attributed to high levels of inflation and squeezed margins as UK plc deals with supply chain inflation and subsequent rise in the cost-of-living. The media sector is also bearing the brunt of these pressures, with advertisers facing higher media costs.

The report, which is the only one to collect advertising revenue data directly from media owners across the entire landscape, shows UK adspend rose by 8.8% in Q2 2022, to a total of £8.6bn, while spend during the first half of the year was up 14.4% at £16.7bn.

The UK’s ad market is forecast to grow by a further 3.9% in 2023, to a total of £36.2bn. This projection represents a downgrade of 0.5pp when compared to the July forecast. Meanwhile, online advertising’s share of total adspend is set to grow to a total of 74.0% for 2022 and is expected to cross the three-quarters threshold (75.2%) in 2023.

The full picture in Q2 2022

The latest data show the continuation of strong recoveries for the out of home (OOH) (+46.4%) and cinema (+2,208.2%) sectors. Further, new IAB figures show online classified advertising – representing recruitment advertising and property listings, among others – was up by almost a third. TV was the only medium to witness a decline in investment during this quarter (-0.6%) though broadcaster video-on demand continued to grow (+9.3%) as audiences turned to catch-up and streaming platforms.

Positive second quarter results were also recorded across the publishing sector, including national newsbrands (+9.1%), magazine brands (+3.3%), and regional newsbrands (+0.6%).

Christmas adspend at record high despite muted lift from World Cup

Adspend for the final quarter of 2022 is set to increase by 4.5% from last year’s record high, to a total of £9.5bn, setting a new record level of investment during the Christmas period. Search advertising – including eCommerce – is forecast to be one of the quickest growing media over the quarter, rising by 7.3% to a total of £3.4bn. At £1.7bn, TV advertising spend is expected to remain flat during the quarter, but video-on-demand is set to rise ahead of the wider market with expected growth of 4.2%.

Stephen Woodford, Chief Executive, Advertising Association commented:

“It is encouraging to see strong figures in Q2, with media channels continuing their recovery from the COVID-19 pandemic. Looking forwards, political and economic stability is much-needed, given the inflationary and recessionary forces impacting all businesses. As companies navigate these pressures, we see them continuing to prioritise advertising investment to protect their brands in exceptionally challenging market conditions.”

James McDonald, Director of Data, Intelligence & Forecasting, WARC commented on the figures: “With the economic picture worsening amid ongoing political incertitude, the likelihood of a recession is now higher than when we last assessed market prospects in the summer. Indeed, we have downgraded UK ad market growth expectations for this year and next, in large part to reflect the waning climate.

“Higher costs are carving into advertisers’ margins and household budgets alike, and trading conditions are at their worst since the Covid outbreak, leading to muted expectations for the Christmas quarter. Against this deteriorating economic backdrop, a 9.2% rise in advertising investment this year would be impressive given that it is near double the average rate of expansion recorded prior to the pandemic.”

Increasing the public’s trust of advertising

The AA/WARC figures for Q2 2022 are released in the same week as a new advertising campaign launches for the Advertising Standards Authority, designed to build the public’s awareness, confidence and trust in advertising and its self-regulatory system. Businesses including Tesco, Marmite, Lloyds, and Churchill feature in the campaign which will run on TV, print, online, cinema and OOH channels over the next three months. The campaign is backed with advertising inventory from media owners including ITV, News UK, Sky, Mail Metro Media, The Guardian, Daily Telegraph, Evening Standard, Channel 4 and Reach plc. In digital media, it will be featured on YouTube, Yahoo, Snapchat and Meta’s channels. Outdoors, the campaign is backed with inventory from Clear Channel, Global, JCDecaux and Ocean Outdoor, and will also see support from DCM and Pearl & Dean in cinemas.

Planned by MediaCom with creative work by Leith Agency, the biggest-ever awareness campaign for the regulator will remind the public and businesses alike that UK ads across media are regulated and that there’s a body to maintain standards and step in when needed.

| Media | Q2 2022

year-on-year % change |

H1 2022 year-on-year % change

|

2022 forecast year-on-year % change | Percentage point (pp) change in 2022 forecast vs July | 2023 forecast year-on-year % change |

| Search | 10.8% | 16.5% | 11.7% | -1.5pp | 6.2% |

| Online display* | 5.4% | 8.1% | 7.1% | -4.3pp | 5.9% |

| TV | -0.6% | 8.7% | 2.9% | -3.0pp | 0.5% |

| of which VOD | 9.3% | 17.2% | 10.1% | -3.2pp | 7.2% |

| Online classified* | 32.4% | 41.4% | 20.1% | +14.5pp | -4.5% |

| Direct mail | 3.8% | 9.5% | 2.8% | +3.0pp | -4.5% |

| Out of home | 46.4% | 79.1% | 31.2% | +2.3pp | 4.8% |

| of which digital | 48.2% | 78.8% | 32.3% | +1.8pp | 8.4% |

| National newsbrands | 9.1% | 12.6% | 3.4% | +2.3pp | -2.5% |

| of which online | 13.2% | 16.3% | 8.2% | +1.6pp | 3.7% |

| Radio | 7.0% | 13.1% | 6.2% | +0.8pp | 0.1% |

| of which online | 5.9% | 14.6% | 8.1% | -2.6pp | 6.3% |

| Magazine brands | 3.3% | 5.0% | 0.7% | +2.0pp | -5.9% |

| of which online | 3.9% | 9.9% | 5.4% | +1.4pp | -1.7% |

| Regional newsbrands | 0.6% | 10.3% | 2.6% | +2.6pp | -7.1% |

| of which online | 5.3% | 13.8% | 7.2% | -0.8pp | -0.5% |

| Cinema | 2,208.2% | 3,978.0% | 174.0% | -17.2pp | 21.1% |

| TOTAL AD SPEND | 8.8% | 14.4% | 9.2% | -1.7pp | 3.9% |

| Note: Broadcaster VOD, digital revenues for newsbrands, magazine brands, and radio station websites are also included within online display and classified totals, so care should be taken to avoid double counting. Online radio includes targeted in-stream radio/audio advertising sold by UK commercial radio companies, together with online S&P inventory. Source: AA/WARC Expenditure Report, October 2022 |

|||||

The Advertising Association/WARC quarterly Expenditure Report is the definitive guide to advertising expenditure in the UK with data and forecasts for different media going back to 1982.

Photo Credit: AA