Growth of £8bn above original forecasts powered by boom in online sector but also increasing cost of advertising

London, April 28, 2022: A new report – UK Advertising’s Adspend Review: The Pandemic Effect – has been published today to mark the definitive full year 2021 Advertising Association/WARC Expenditure Report figures, which show the extraordinary adspend growth seen during the recovery from the Covid-19 pandemic.

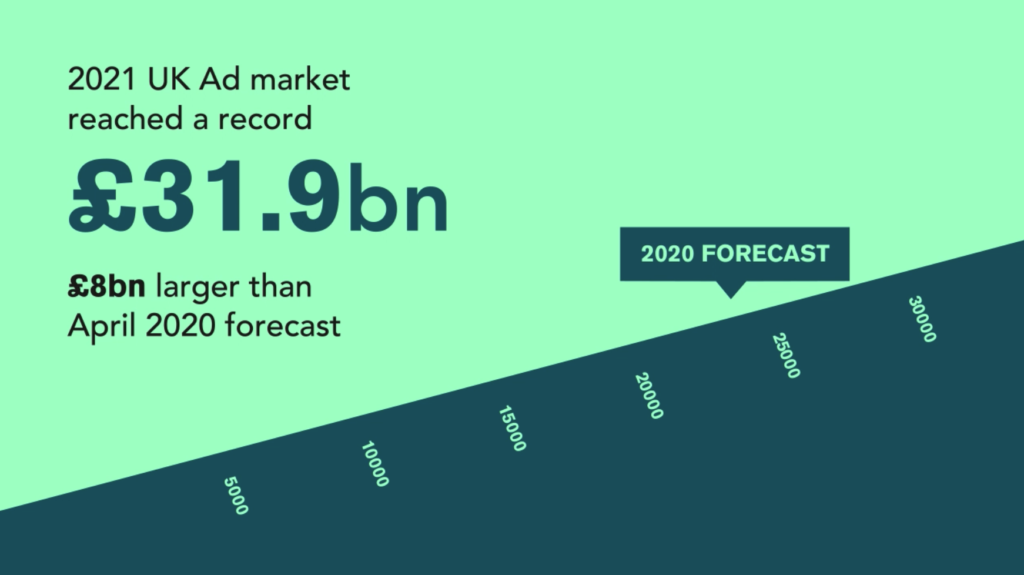

The UK ad market reached a record £31.9bn in 2021, equating to growth of 34.3% year-on-year. The latest AA/WARC full year figures reveal the 2021 ad market emerged £8bn larger than April 2020’s original forecast of £24bn set at the beginning of the Covid-19 pandemic. This growth is in part due to inflationary pressures on the cost of advertising but also a higher-than-expected growth in key forms of online advertising during the past year.

Three in every four pounds spent on UK advertising today is invested in one of a wide range of online formats – only China has an equivalent online share of this proportion. New data shows internet adspend totalled £23.5bn in 2021, equivalent to 73.5% of all UK adspend and a jump up of 11.7 percentage points from pre-pandemic levels in 2019.

Notable shifts were seen in adspend, sector by sector, during the pandemic with the UK Government quickly becoming the UK’s largest advertiser to drive mass behaviour change. This shift is further examined in ‘UK Advertising’s Adspend Review: The Pandemic Effect’. It includes contributions from WARC, the global authority on advertising and media effectiveness; Credos, UK advertising’s thinktank; and industry perspectives from AA members, including Google, Tesco, News UK, UM, ISBA, as well as TV marketing body, Thinkbox. The review also notes the pandemic has seen a disruption in the usual relationship between GDP and adspend.

Forecasting the years ahead

The latest AA/WARC data presents an upgrade to the previous forecasts for 2022. The UK’s ad market is forecast to grow by 10.7% this year to £35.3bn, driven by a strong start to the year, higher CPMs and higher demand ahead of the FIFA World Cup. In 2023, this is set to add an additional 5.4% year-on-year to reach £37.2bn, though economic headwinds – particularly in relation to cost of living pressures and supply chain disruption – mean this is liable to review.

Online threshold marks a new era of advertising

The latest AA/WARC figures show search, inclusive of e-commerce, proved to be the strongest performer in 2021 – at £11.7bn it beats April 2020’s projection (made during the onset of the Covid-19 pandemic) by over £3.7bn. In addition, TV surpassed early expectations by almost £1bn, while online video overperformed by approximately £2bn and social media by £2.3bn in relation to the forecasts made at the start of the pandemic.

The UK Advertising’s Adspend Review also contains commentary from Credos, highlighting the close link between internet retail spend and online adspend. With online retail spend of $2,648 per capita, the UK has the world’s most avid online shoppers. In tandem, the UK ad industry is seeing an exponential demand for digital skills and talent to serve this demand.

Commentary from WARC concludes that the changes seen in the advertising market during the pandemic allude to an emerging structural shift, one which points to a new era of advertising with retail media poised to play a more prominent role in future.

Stephen Woodford, Chief Executive, Advertising Association, said: “The UK has held its position in 2021 as the largest advertising market in Europe through the pandemic and is now the third largest in the world, behind the USA and China. While further growth is forecast, inflationary pressures on the cost of advertising, and more generally, due to the ongoing geo-political uncertainties, mean we should be cautious.

“While lockdowns saw sharp declines in spend across some sectors, the pandemic presented our industry with opportunities to innovate and meet the public health challenges. The UK Government remained in pole position as the largest advertiser. Cover wraps in our print media informed the nation with ‘Stay Home’ public health messages; direct mail brought testing kits and essential deliveries to households up and down the country; and billboards showed the everyday heroes in our NHS.

“Such innovation, creativity and responsiveness will be critical in the years going forward, as we build a sustainable future for our industry, and help businesses, large and small, build relationships with their customers.”

James McDonald, Director of Data, Intelligence & Forecasting, WARC said: “The Covid-19 recovery last year was buoyed in part by the release of pent-up investment on established online platforms – as well as maturing ones such as TikTok – and in part by the emergence of retail media as a major contender for marketing budgets. The latter trend bears the hallmark of a new era in advertising, one which is set to fuel growth over the forecast period and beyond.

“Be that as it may, economic headwinds create uncertainty ahead; the consumer is being stretched further than at any other time since the Second World War, conflict in Europe has stoked market volatility and has exacerbated supply chain pressures, and the prospect of a UK recession cannot be ignored. Given the market’s current momentum, however, we do not yet see this translating into an advertising recession over the coming quarters.”

The Advertising Association/WARC quarterly Expenditure Report is the definitive guide to advertising expenditure in the UK with data and forecasts for different media going back to 1982.

| Media | 2020 £m |

2021 £m |

2021 year-on-year% change |

2022 forecast year-on-year

% change |

2023 forecast year-on-year

% change |

| Search | 8,418.2 | 11,658.6 | 38.5% | 12.2% | 7.8% |

| Online display* | 7,308.5 | 10,759.0 | 47.2% | 11.6% | 7.4% |

| TV | 4,398.0 | 5458.0 | 24.1% | 7.1% | 2.0% |

| of which BVOD | 522.7 | 732.8 | 40.2% | 14.5% | 10.5% |

| Online classified* | 975.6 | 1,053.4 | 8.0% | 3.0% | -4.7% |

| Direct mail | 909.0 | 1,082.0 | 19.0% | -4.1% | -7.0% |

| Out of home | 699.1 | 901.3 | 28.9% | 31.5% | 8.6% |

| of which digital | 414.9 | 576.8 | 39.0% | 34.3% | 11.5% |

| National newsbrands | 744.3 | 846.0 | 13.7% | 1.0% | -2.8% |

| of which online | 301.3 | 369.6 | 22.7% | 4.5% | 0.9% |

| Radio | 577.1 | 718.7 | 24.5% | 3.1% | 3.8% |

| of which online | 46.8 | 71.3 | 52.2% | 11.1% | 9.4% |

| Regional newsbrands | 469.3 | 510.5 | 8.8% | -4.8% | -7.3% |

| of which online | 183.3 | 250.9 | 36.9% | 3.6% | -0.2% |

| Magazine brands | 462.6 | 556.4 | 20.3% | -1.6% | -5.3% |

| of which online | 200.1 | 297.7 | 48.8% | 1.5% | -2.1% |

| Cinema | 55.1 | 102.8 | 86.6% | 213.0% | 11.5% |

| TOTAL UK ADSPEND | 23,762.6 | 31,924.4 | 34.4% | 10.7% | 5.4% |

| Note: Broadcaster VOD, digital revenues for newsbrands, magazine brands, and radio station websites are also included within online display and classified totals, so care should be taken to avoid double counting. Online radio includes targeted in-stream radio/audio advertising sold by UK commercial radio companies, together with online S&P inventory.

Source: AA/WARC Expenditure Report, April 2022 |

|||||