Latest figures mark 24th consecutive quarter of market growth

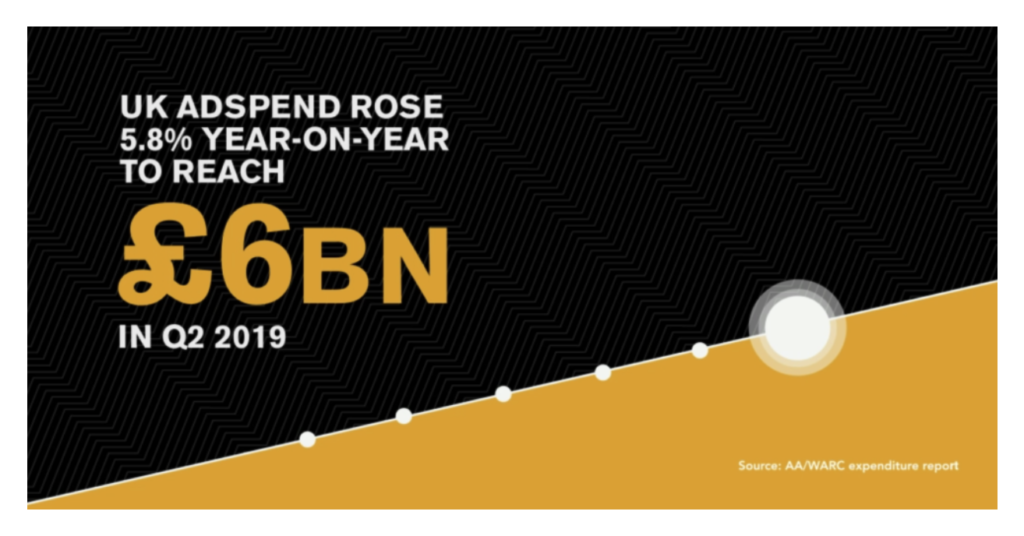

UK adspend rose 5.8% year-on-year to reach £6.0bn in Q2 2019, marking UK advertising’s 24th consecutive quarter of market growth. Adspend over the first six months of 2019 was 5.2% higher than a year earlier, at £12.0bn. These figures are contained within today’s Advertising Association/WARC Expenditure Report, which is unique in its collection of advertising spend data from across the entire media landscape.

The report shows adspend growth for 2019 is forecast to rise 5.0% and reach £24.7bn, with the UK’s ad market expected to grow a further 5.3% in 2020. The predicted full year growth figure for 2019 is an upgrade of 0.4 percentage points on the figure forecast at the last release of adspend data in July this year.

Overall market growth is being driven by increased spend on online advertising, which saw rises across most formats. Digital ad formats for radio broadcasters witnessed a year-on-year rise of 15.9% and online national newsbrands recorded growth of 15.6% over the same period. Digital out of home – not included in online totals – experienced growth of 17.2%.

The report reveals particularly strong growth in Q2 2019 compared to Q2 2018 in TV video on demand (VOD) and cinema. TV VOD saw an increase of 20.0% in Q2 2019 while cinema recorded a very impressive rise of 49.6%. The sector benefited from the entry of a number of new advertisers in comparison to the same period in 2018, boosting growth substantially.

Stephen Woodford, Chief Executive, Advertising Association commented:

“These very encouraging adspend figures for Q2 2019 cover the period immediately following the original Brexit date of March 29, demonstrating the continued strength of UK advertising during a time of political uncertainty. Advertising’s dynamism is shown by the growth recorded across many different formats, with particularly impressive performances from cinema, TV VOD and online radio.

“These figures are positive for our industry and are good indicators of the resilience of the UK economy. However, with another scheduled Brexit departure date looking likely to be passed on 31 October, we are acutely conscious of industry’s desire for the clarity needed to continue investing for the future during these uncertain times.”

James McDonald, Managing Editor at WARC commented

“An upgrade to our 2019 projection of almost half a point is reflective of stellar online growth, as well as over-performance for a number of traditional channels against the expectations we laid out in July. There is little in the data we receive from media owners across the industry to suggest an impending downturn, but growth cannot be taken for granted while economic prosperity remains in the balance.”

| Full-year forecast summary 2018-2020 | Adspend 2018 (£m) | 2018 v 2017 (% change) | Forecast 2019 (Year-on-year

% change) |

Forecast 2020 (Year-on-year

% change) |

| Search | 6,656 | 14.3% | 11.6% | 10.3% |

| Online display* | 5,332 | 21.4% | 13.1% | 10.1% |

| TV | 5,111 | 0.1% | -0.9% | 2.5% |

| of which VOD | 391 | 29.4% | 18.7% | 15.0% |

| Direct mail | 1,552 | -8.7% | -9.5% | -5.4% |

| Online classified* | 1,451 | -1.3% | 1.3% | 1.8% |

| Out of home | 1,209 | 5.7% | 6.9% | 3.7% |

| of which digital | 603 | 14.7% | 13.4% | 11.7% |

| National newsbrands | 968 | -7.1% | -3.5% | -3.6% |

| of which online | 274 | -2.6% | 5.0% | 5.4% |

| Regional newsbrands | 804 | -9.3% | -9.3% | -4.6% |

| of which online | 228 | 7.6% | 5.4% | 7.0% |

| Magazine brands | 718 | -7.5% | -7.6% | -5.0% |

| of which online | 270 | -0.3% | -1.4% | 0.3% |

| Radio | 714 | 5.1% | 2.7% | 4.8% |

| of which online | 45 | 30.6% | 20.4% | 21.2% |

| Cinema | 254 | -2.1% | 16.4% | -3.2% |

| TOTAL UK ADSPEND | 23,561 | 6.2% | 5.0% | 5.3% |

| * Broadcaster VoD, digital revenues for newsbrands, magazine brands, and radio station websites are also included within online display and classified totals, so care should be taken to avoid double counting.

Source: AA/WARC Expenditure Report, October 2019 |

||||

| At-a-glance media summary | Q2 2019 v Q2 2018 | Actual versus forecast |

| % change | Percentage points (pp) | |

| Search | 12.7% | +3.3pp |

| Online display* | 11.0% | -1.2pp |

| TV | 1.3% | = |

| of which VOD | 20.0% | +1.1pp |

| Direct mail | -14.4% | -3.9pp |

| Online classified* | 8.9% | +6.3pp |

| Out of home | 9.4% | +4.3pp |

| of which digital | 17.2% | +4.1pp |

| National newsbrands | 0.3% | +5.9pp |

| of which online | 15.6% | +12.2pp |

| Regional newsbrands | -11.3% | -2.9pp |

| of which online | 7.3% | +5.4pp |

| Magazine brands | -6.2% | = |

| of which online | -2.6% | -0.4pp |

| Radio | 3.3% | -0.4pp |

| of which online | 15.9% | -6.2pp |

| Cinema | 49.6% | +44.5pp |

| TOTAL UK ADSPEND | 5.8% | +1.3pp |

| * Broadcaster VoD, digital revenues for newsbrands, magazine brands, and radio station websites are also included within online display and classified totals, so care should be taken to avoid double counting.

Source: AA/WARC Expenditure Report, October 2019 |

||

The full report and tables can be accessed through the WARC website for an annual subscription fee.