New forecasts show ad market’s value is set to reach £38.8bn this year and top £40bn by 2025.

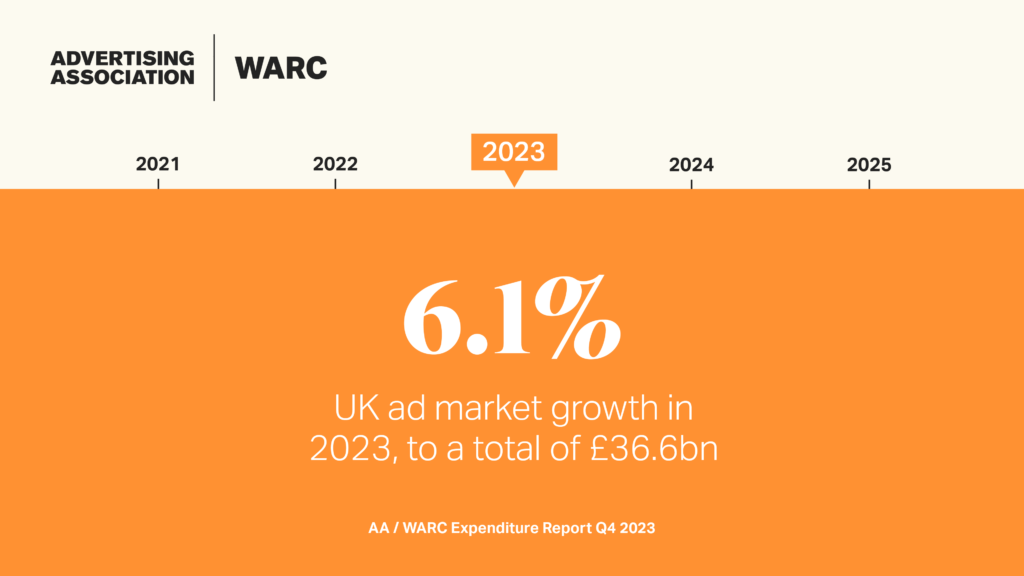

London, April 25, 2024: The latest Advertising Association/WARC Expenditure Report, published today, shows that the UK’s ad market recorded a 6.1% increase in investment to a total of £36.6bn in 2023; the 13th annual expansion recorded in the last 14 years. The new survey data also shows that online formats now account for over three-quarters of all UK ad spend for the first time.

New AA/WARC forecasts show advertising spend will rise by 5.8% to reach £38.8bn this year, though this represents a minor (-0.1pp) downgrade from January’s forecast owing to prolonged inflationary pressures on the market. Further growth – of 4.5% – is expected in 2025, by when the UK’s ad market will be worth more than £40bn.

When compared to Europe’s largest advertising markets, the UK’s advertising industry was seen to have outpaced Germany (-0.7%), France (+2.1%) and Ireland (+3.0%) last year, and is expected to repeat this in 2024. The UK’s ad market is on course to end the year some $20bn larger than those of its closest neighbours.

The full picture in 2023

While UK ad spend grew by 6.1% last year, this equated to a 1.2% contraction in real terms after accounting for high inflation, a rate which slightly lagged the flat (+0.1%) activity witnessed across the UK’s economy last year.

As estimated in January, online formats combined grew by 11% to reach a total of £28.7bn in 2023, equivalent to 78.4% of all UK ad spend last year. Beyond this, out of home (+9.7%) was the only other advertising medium to record growth in 2023.

The only major product sectors to record rising display ad spend (i.e. excluding search and classified formats) last year were retail (+5.0%) and services (+4.7%), the latter almost entirely attributable to a 6.6% rise in the entertainment & leisure sector.

The latest AA/WARC data also reveals actual investment for last year’s Q4 Christmas ad season, which topped £9.7bn after achieving growth of 7.4% year-on-year. This growth was led by digital out-of-home (+18.1%) and BVOD (+15.9%) as well as search (+12.9%), as the traditional uplift in Golden Quarter investment was buoyed further by increased advertising activity during the Rugby World Cup.

Projections for 2024 and 2025

The latest AA/WARC dataset expects the UK advertising market to grow 5.8% to reach nearly £39bn in 2024. Broadcast media, most notably TV (+2.6%) and radio (+2.3%) are expected to return to growth, while the same is true for cinema (+2.5%). Among digital formats, search (+8.9%) and online display (+6.4%) are again set to see the strongest rises, closing the year with a combined share of 77% of all spend.

More favourable economic conditions should encourage advertisers to invest more in brand-building campaigns in 2024 and this, coupled with short-term stimuli such as the Men’s Euros in June, the upcoming General Election in the second half of the year and, to a lesser extent, the Paris Olympics in July, are expected to contribute to healthy growth in formats such as broadcaster video-on-demand (+14.1%) this year.

The picture is set to improve further for more channels in 2025 as a rise of 4.5% is forecast for the market as a whole. This includes an 11% rise for BVOD, 6.4% for search and 5.5% for online display, as economic headwinds are anticipated to ease.

Stephen Woodford, Chief Executive, Advertising Association said: “The continued shift to online advertising formats reflects the changing shape of our economy, with people increasingly shopping online as well as on the high street, and businesses striving to provide the best customer experience in all scenarios. The UK advertising industry is much respected around the world, which is why we continue to see the exports of UK advertising services grow, an important source of additional revenue for many advertising businesses in a domestic economy that has little-to-no growth.”

James McDonald, Director of Data, Intelligence & Forecasting, WARC said: “Our latest survey of media owners confirms 2023 as a challenging year for most, with few properties recording gains and spend instead further consolidating within search and online display formats – particularly social media. Combined, these digital staples are on course to account for almost four in five pounds spent on advertising in the UK next year, up from a share of 51% just five years ago.

“Our forecasts assume that the UK’s economy will begin to break from the pattern of stagnation that has come to define recent quarters. Easing inflation over the coming 18 months should encourage more favourable trading conditions within the advertising sector, facilitating growth across a broader range of channels in turn.”

| Media | 2022 £m |

2023 £m |

2023 year-on-year % change |

2024(f) year-on-year % change |

2025(f) year-on-year % change |

| Search | 13,143.8 | 14,705.0 | 11.9% | 8.9% | 6.4% |

| Online display* | 11,612.2 | 12,925.1 | 11.3% | 6.4% | 5.5% |

| TV | 5,381.0 | 4,900.0 | -8.9% | 2.6% | 0.9% |

| of which BVOD | 845.4 | 979.6 | 15.9% | 14.1% | 11.0% |

| Out of home | 1,181.2 | 1,295.3 | 9.7% | 7.2% | 5.6% |

| of which digital | 749.9 | 841.3 | 12.2% | 9.5% | 7.3% |

| Online classified | 1,110.8 | 1,080.8 | -2.7% | -0.6% | 1.5% |

| Direct mail | 1,094.5 | 956.7 | -12.6% | -4.9% | -3.3% |

| National newsbrands | 825.3 | 773.6 | -6.3% | -3.3% | -2.1% |

| of which online | 374.5 | 352.8 | -5.8% | -0.8% | 0.8% |

| Radio | 740.1 | 715.5 | -3.3% | 2.3% | 1.6% |

| of which online | 77.7 | 72.2 | -7.1% | 7.5% | 4.1% |

| Magazine brands | 553.8 | 503.3 | -9.1% | -5.1% | -0.8% |

| of which online | 302.2 | 260.8 | -13.7% | -4.8% | 2.0% |

| Regional newsbrands | 505.2 | 454.2 | -10.1% | -3.3% | -2.0% |

| of which online | 259.2 | 239.4 | -7.6% | -1.7% | 0.2% |

| Cinema | 229.5 | 219.9 | -4.2% | 2.5% | 2.2% |

| TOTAL UK ADSPEND | 34,518.5 | 36,624.3 | 6.1% | 5.8% | 4.5% |

| Note: Broadcaster VOD, digital revenues for newsbrands, magazine brands, and radio station websites are also included within online display and classified totals, so care should be taken to avoid double counting. Online radio includes targeted in-stream radio/audio advertising sold by UK commercial radio companies, together with online S&P inventory. Source: AA/WARC Expenditure Report, April 2024 |

|||||

The quarterly Advertising Association/WARC Expenditure Report is the definitive guide to advertising expenditure in the UK, with data for all key advertising media and sub formats dating back to 1982 and forecasts spanning eight quarters ahead.