Member content

Already a member? Sign in below

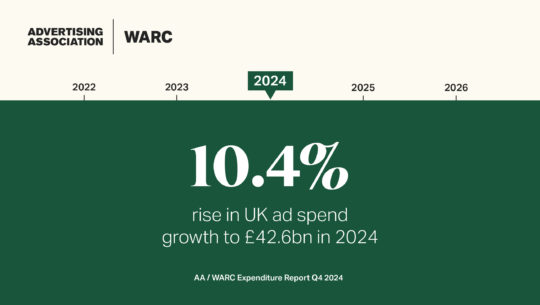

UK adspend rose 6.4% year-on-year to reach £5.6bn in Q2 2018 – the 20th consecutive quarter of market growth. Coupled with an overall adspend rise of 7.2% year-on-year during the first half of 2018, to a total of £11.4bn, this was both the strongest second quarter and first half since 2014.

This record investment, highlighted in Advertising Association/WARC Expenditure Report data, published today, means full-year outlooks for 2018 and 2019 have been upgraded to +6.3% and +4.9% respectively. This would lead to a projected adspend total of over £23.5bn for 2018.

Overall market growth is being driven by increased spend on online advertising. Internet advertising – inclusive of online revenues for newsbrands, magazine brands, broadcaster video-on-demand and radio station websites – continues to grow at a rapid rate and consequently full-year projection figures have been upgraded by three and a half points to 13.3% growth this year. This would result in over £13bn being spent on online advertising in the UK this year.

Data show that mobile accounted for over half of search spend for the first time in the second quarter. Further, display formats are also growing strongly – online video attracted half a billion pounds during the three months to end-June.

The TV market grew ahead of expectations in the second quarter of 2018, with total spend rising 1.9% to £1.2bn. Spot advertising – 89% of the total – rose for the third consecutive quarter, and the 1.4% growth rate was ahead of forecast.

The figures come as the UK Government seeks to come to an agreement with EU on Brexit and are based on a positive outcome to negotiations, as is sought by both sides.

Minister for Digital and the Creative Industries Margot James said:

“It’s fantastic to see our world leading advertising sector continuing to flourish. The industry makes a huge contribution to the UK economy, and its international reputation for creative excellence is playing a vital role in helping to bang the drum for Britain abroad.”

Stephen Woodford, Chief Executive at the Advertising Association commented:

“Spend on advertising is showing real strength and resilience especially at a time of some uncertainty for UK business. We know advertising has a positive effect on the economy, with £1 spent generating £6 for UK GDP, so it is encouraging to see the strongest Q2 and H1 results since 2014.

“While we welcome these figures, we are also conscious that our upgraded predictions for 2018 and 2019 depend on getting the right deal from Brexit negotiations and clarity on what the future will look like.

“We must also ensure that the unique features that have made the UK the global hub for our industry, such as access to the best and brightest creative talent from across the world, are prioritised as we leave the EU.”

James McDonald, Data Editor at WARC said:

“Growth in online advertising spend continues to exceed our expectations, resulting in the fifth upgrade to our forecasts in as many quarters. Barring any major shock to the system, this trend should continue to play out over the years ahead, lifting total market value in tow.”

|

Full-year forecast summary |

Adspend 2017 (£m) | 2017 v 2016 | Forecast 2018 | Forecast 2019 |

| % change | % change | % change | ||

| Internet* | 11,553 | 14.3% | 13.3% | 9.6% |

| of which mobile | 5,223 | 37.3% | 27.9% | 19.5% |

| TV | 5,108 | -3.2% | 1.4% | 0.8% |

| of which VoD | 211 | 7.1% | 10.5% | 9.5% |

| Direct mail | 1,700 | -3.1% | -4.5% | -3.8% |

| Out of home | 1,144 | 1.5% | 3.3% | 3.6% |

| National newsbrands | 1,033 | -5.5% | -4.3% | -3.3% |

| of which digital | 275 | 19.3% | 3.5% | 6.3% |

| Regional newsbrands | 887 | -13.1% | -8.0% | -4.1% |

| of which digital | 212 | 9.9% | 11.4% | 9.7% |

| Magazine brands | 776 | -11.5% | -8.5% | -6.5% |

| of which digital | 271 | -4.0% | -1.1% | -1.6% |

| Radio | 679 | 5.2% | 6.8% | 5.1% |

| of which digital | 35 | 26.3% | 25.0% | 16.7% |

| Cinema | 259 | 2.7% | 3.9% | 7.0% |

| TOTAL UK ADSPEND | 22,137 | 4.3% | 6.3% | 4.9% |

| * Broadcaster VoD, digital revenues for newsbrands and magazine brands, radio station websites and mobile advertising spend are also included within the internet total of £11,553m, so care should be taken to avoid double counting. Source: AA/WARC Expenditure Report, November 2018 |

||||

| At-a-glance media summary – Q2/H1 2018 | Q2 2018 v Q2 2017 | H1 2018 v H1 2017 |

| % change | % change | |

| Internet* | 14.5% | 14.8% |

| of which mobile | 29.2% | 30.4% |

| TV | 1.9% | 3.5% |

| of which VoD | 9.4% | 10.8% |

| Direct mail | -4.1% | -5.0% |

| Out of home | 1.5% | 3.3% |

| National newsbrands | -7.4% | -4.2% |

| of which digital | 3.6% | 3.2% |

| Regional newsbrands | -9.6% | -9.3% |

| of which digital | 9.7% | 14.0% |

| Magazine brands | -9.0% | -8.7% |

| of which digital | 6.2% | 1.1% |

| Radio | 1.9% | 7.1% |

| of which digital | 20.4% | 29.2% |

| Cinema | -2.4% | -7.8% |

| TOTAL UK ADSPEND | 6.4% | 7.2% |

| * Broadcaster VoD, digital revenues for newsbrands and magazine brands, radio station websites and mobile advertising spend are also included within the internet total, so care should be taken to avoid double counting. Source: AA/WARC Expenditure Report, November 2018 |

||

Already a member? Sign in below

If your company is already a member, register your email address now to be able to access our exclusive member-only content.

If your company would like to become a member, please visit our Front Foot page for more details.

Enter your email address to receive a link to reset your password

Your password needs to be at least seven characters. Mixing upper and lower case, numbers and symbols like ! " ? $ % ^ & ) will make it stronger.

If your company is already a member, register your account now to be able to access our exclusive member-only content.