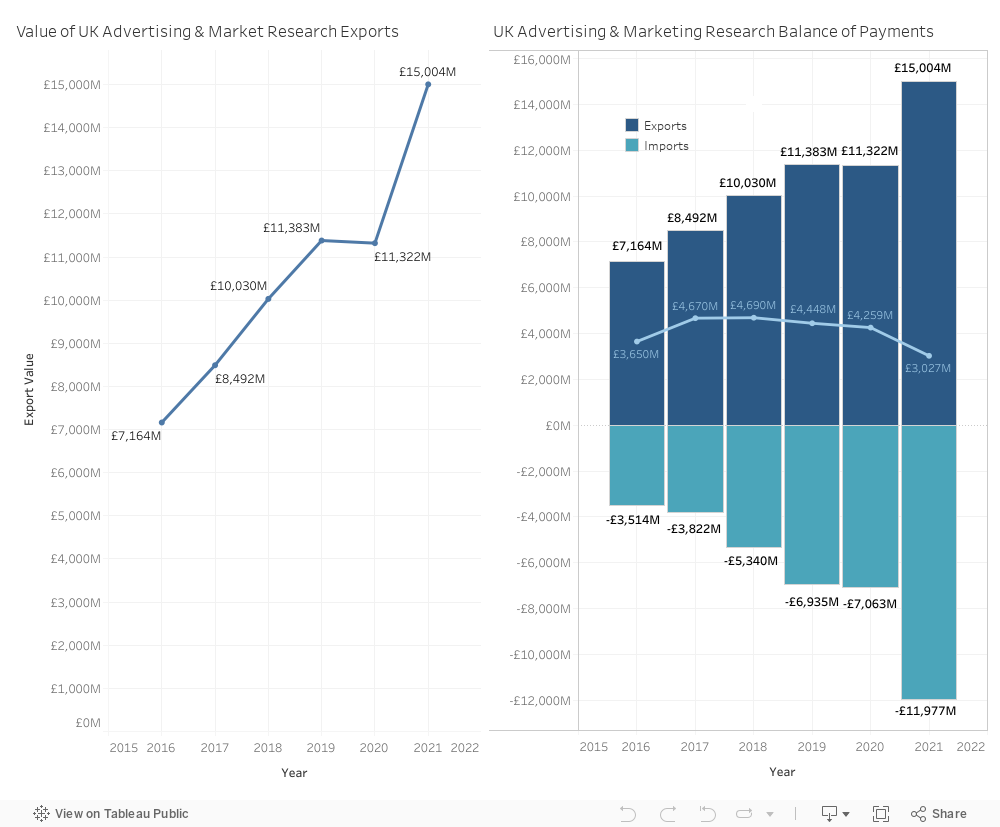

The latest release of data from the Office for National Statistics’ (ONS) UK Trade in Services survey attributed an annual figure of £15 billion to advertising and market research services exports for the year ending 31 December 2021.

This data references the ONS UK trade in services: service type by partner country, non-seasonally adjusted [1] dataset which is updated on a quarterly basis. Services trade covers any type of services industry including advertising and marketing, legal services, engineering services among others. Figure 1 shows the value of UK exports of advertising, marketing and opinion polling services to the rest of the world and the balance of payments.

Figure 1. Value of UK Advertising & Marketing Research Exports on annual basis (left side) and balance of payments (right side). Note that the data has been revised by the ONS hence some figures are higher, and in some cases lower, compared to last year’s report. Source: ONS UK trade in services: service type by partner country, non-seasonally adjusted (Released: 26 January 2023)

Note that the ONS uses the international EBOPS (Extended Balance of Payments Services classification) standard for publishing data for our sector (See Annex A for further detail).

This figure represents a remarkable 32.5% growth year-on-year – the single largest year of growth since we have been tracking these results.

Explanations

While we do not have enough granular data currently to explain with confidence what was behind this remarkable growth, we do offer some possible explanations and context for 2021’s figures.

The first potential factor is the shift towards online retail, and the consequent increase in digital ad spend. In last year’s exports report we noted the strong pivot towards online retail and how strong consumption signals via this channel led to an increased demand for advertising. This seems to have been borne out by the figures published by the IAB UK, which showed that digital ad spend grew 41% to £23.47 billion in 2021 [2].

The increase in digital ad spend and significantly higher exports is arguably a reflection of the UK adapting to a new environment and getting better at delivering services online. However, increased digital ad spend may also in part explain the sharp rise in imports in 2021; sales by digital platforms such as Google and Meta to UK-based companies are counted by ONS as an import because the UK company is purchasing advertising space/time from a foreign company. The balance of payments (the difference between exports and imports) remains positive at £3 billion but this is nearly a 30% decline compared to 2020 as imports seem to have increased significantly by 70%.

The second potential cause is the phased removal of COVID restrictions throughout 2021 and the return to in-person events and travel overseas. This is because services that are provided in the UK to foreign visitors can also be classed as an export. For example, an international advertising and marketing event hosted in the UK (assuming the event host is a UK company) which attracts foreign visitors can be classed as consumption abroad so it would register as an export for the UK but an import for the visitor’s home country. This nuance within trade definitions may go some way to explaining the sharp rise in exports in Q4 of 2021, coinciding with the least restricted period of the year.

Quarterly breakdown

Analysis of the quarterly data in Figure 2 showed that the export value in each quarter of 2021 was the highest on record. There was also a strong start during the first two quarters 2022, carrying on this positive trajectory. At the time of writing, Q4 2022 data had yet to be published but current indications suggest that export growth may have peaked, and we can expect some moderation towards the end of 2022.

However, it is important to note that these numbers are subject to revision by the ONS. This was the case last year when it initially appeared that exports might experience serious headwinds in 2021. It is also worth noting the consistent trend of Q4 being significantly higher for export value, with each year showing dips or stagnation between Q2 and Q3 before large jumps in Q4. This is likely a seasonal feature of advertising exports, and we think it is due to increased spend in the lead up to Christmas. We therefore may see a different picture in next year’s export report, in light of revised figures and the inclusion of the key fourth quarter.

Figure 2. Quarterly Analysis of Advertising and Market Research exports. Source: ONS UK trade in services: service type by partner country, non-seasonally adjusted (Released: 26 January 2023)

Regardless, there are indications that the global advertising industry is facing some challenges, and this may reflect UK prospects for 2022 and beyond. For example, Meta laid off 11,000 from its global workforce after announcing Q3 2022 revenues fell by 4%, to USD27.71 billion. This is significant as most of the Meta’s revenue is generated from advertising. Additionally, YouTube fourth quarter earnings missed analyst expectations by posting advertising revenues of USD7.96 billion vs. USD8.25 billion expected. In slightly contrasting fortunes WPP’s full year 2022 revenues were up 13% compared to 2021 but profit margin was slightly down at 4.7% from 5% in 2021 due to higher expenses.

References

[1] https://www.ons.gov.uk/businessindustryandtrade/internationaltrade/datasets/uktradeinservicesservicetypebypartnercountrynonseasonallyadjusted

[2] https://www.iabuk.com/adspend