Inflation continues to be a general concern, both domestically and globally, with pent-up demand from the pandemic, tightness in the labour market, supply chain disruptions, and the war in Ukraine all contributing to rising prices. As a result, central banks have engaged in monetary tightening since 2022 to rein in inflation.

Real terms value adjusts export value to take inflation into account, making it a better guide to growth in exports as it removes price effects that may distort the data.

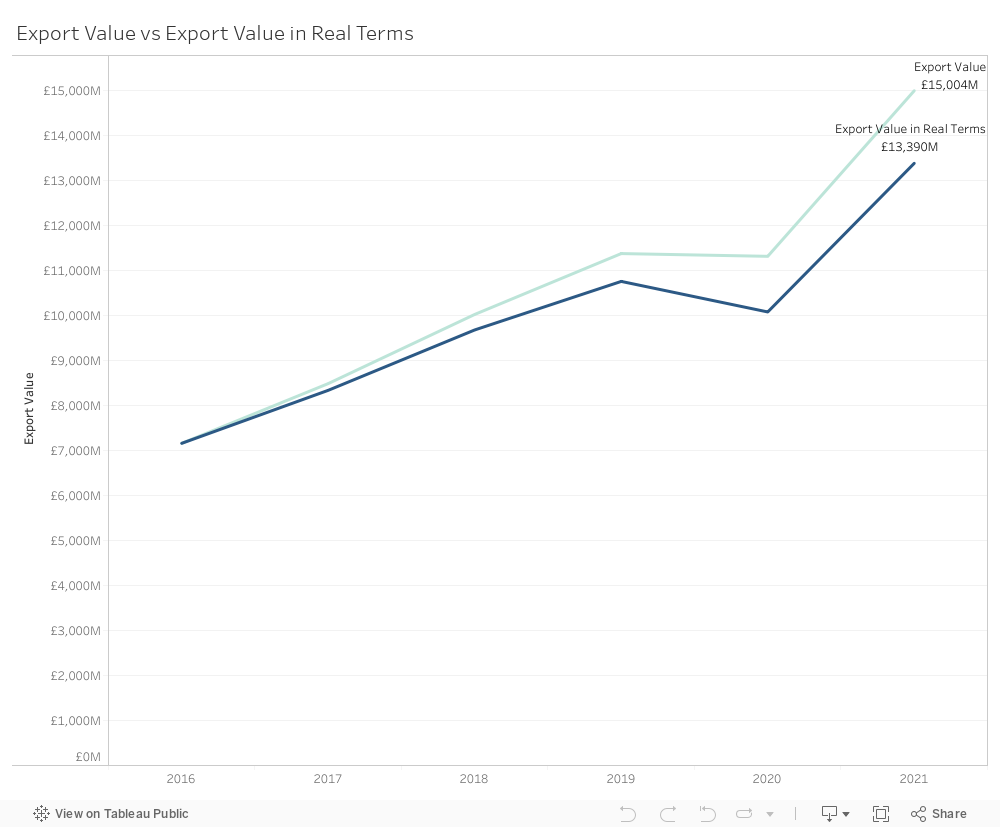

Here, we examine the effect of inflation on export value growth using a GDP deflator (See Annex B). The GDP deflator can be viewed as a measure of general inflation in the domestic economy and can be used to determine export growth in real terms (Figure 3).

Using 2016 as the base, the actual and real terms lines diverge over time, with the rate of divergence being most significant in 2020 and 2021. In 2021 the difference between actual and real terms export growth reached 12%.

Considering the rate of inflation throughout 2022, we assume the lines will start to diverge far more dramatically once we have the full results for 2022.

Inflation and interest rates

To combat inflation, many central banks across the world, including the Bank of England, have embarked on a path of monetary tightening. Monetary policy includes several policy tools but the key one is interest rates due to its direct effect on consumers, requiring borrowers to pay more in interest payments on loans and savers to earn more for deposits.

Although inflation is expected to fall from its current highs by the middle of the year, particularly as energy prices have fallen, there is some concern that inflationary pressures will remain at persistently high levels. At the time of writing, the Federal Reserve and European Central Bank have taken a more hawkish tone and are indicating further interest rate rises this year. A member of the Bank of England’s monetary policy committee indicated that to get the UK to its 2% target annual inflation rate interest rates would be need to rise further from their current 4% level.

Exchange rate impact

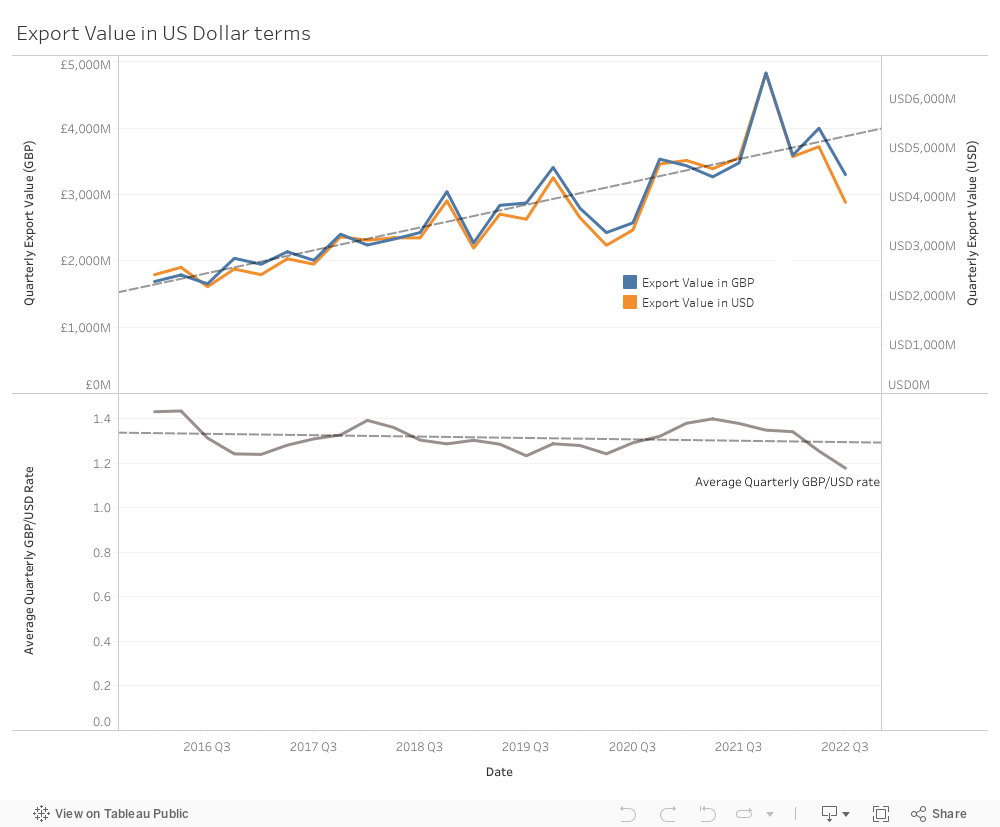

One effect of interest rate movement is its impact on exchange rates. For example, if the Federal Reserve increases its base rate, it tends to make dollar-denominated bonds and interest-rate linked products more attractive and hence the dollar stronger. Some argue that a lower exchange rate relative to the dollar may help export competitiveness in the short run.

The top chart in Figure 4 shows the comparison of quarterly export values in GBP and USD terms. The bottom chart is a time series of the average quarterly GBP/USD exchange rate.

From 2016, we see that there is a positive overall trend of quarterly export values, which is increasing over time. However, there is also a gradual decline in the exchange rate between the GBP and USD. In practical terms, the pound exchanging for less dollars means that UK exports are cheaper when priced in USD.

From the data, there does not seem to be any negative impact on the growth of exports. However, this will be little consolation to importers and companies who report revenue in USD.

From 2018 onwards, there has been increasing volatility in the quarterly numbers, with simultaneous declines in export value and exchange rate recorded around Q3 2022 being particularly noticeable. Greater volatility can make it difficult for buyers to plan and optimise value (why buy today if prices might be cheaper tomorrow?). That said, given that the numbers are subject to revision it is too early to say for certain what effect the sharper decline in GBP/USD rates in Q3 2023 had on exports. We will know with greater certainty in our next report.